While a temporary, limited de‑escalatory step has occurred this week, no material improvement has yet translated into stable or predictable transport operations across air or ocean networks.

Airspace restrictions, maritime corridor disruption, elevated insurance costs, and sustained fuel price pressure continue to affect global logistics flows. The impact remains most pronounced across Asia–Europe, Europe–Middle East, and trans‑Gulf trade lanes. As the disruption extends in time, secondary effects are becoming increasingly structural, particularly across Asia–North America and Europe–North America corridors, affecting capacity availability, transit times, reliability, and pricing.

Air freight – Capacity & Network Status

Air cargo operations in and around the Middle East remain severely constrained, with conditions broadly unchanged versus last week.

- Selected Gulf carriers (including Emirates, Etihad, and Qatar Airways) continue to operate restricted, tightly controlled movements, primarily for aircraft repositioning, repatriation, and pre‑approved freighter services.

- These operations remain subject to regulatory oversight, controlled routings, fuel stops, and short‑notice cancellations.

- The majority of belly and freighter capacity via traditional Gulf hubs remains unavailable for routine cargo planning.

- Dubai (DXB/DWC), Abu Dhabi (AUH), and Doha (DOH) cannot yet be considered reliable cargo hubs and continue to operate on a case‑by‑case approval basis.

- Regional air cargo capacity through the Gulf remains approximately 30% below pre‑conflict levels, with no meaningful recovery observed.

Cargo operations across the UAE remain under sustained pressure. Persistent backlogs continue in Dubai and Sharjah, with overflow pressure increasingly absorbed by Abu Dhabi. Booking remains subject to carrier approval, and frequent last‑minute schedule changes should be expected.

Surface transport limitations into Qatar also continue to constrain road‑based contingency options. Gulf hub routings and cross‑border trucking should not be assumed as reliable fallback solutions.

Middle East Airspace & Operational Environment

The regional operating environment remains fluid and operationally fragile.

- Iran, Iraq, Kuwait, and Syria remain closed or effectively unavailable for routine civilian traffic.

- Israeli airspace remains highly restricted, with limited, government‑approved movements only.

- UAE and Qatari airspace remain partially open via strictly controlled corridors, with capacity caps and case‑by‑case approvals.

- Saudi Arabia and Oman continue to serve as critical transit corridors, operating under contingency routings and elevated ATC load.

- Jordanian airspace remains restricted and subject to short‑notice operational changes.

Even where corridors remain technically open, operational reliability and uplift availability remain inconsistent and should not be assumed for routine planning.

Maritime Chokepoints – Strait of Hormuz, Red Sea & Bab el‑Mandeb

What changed this week:

- Iran and the United States agreed to a temporary two‑week ceasefire.

- Despite this, the Strait of Hormuz remains effectively “permission‑based”, with vessel movements controlled by the IRGC.

- Vessel transits remain very limited and highly selective, and several commercial vessels were still damaged or hit immediately prior to the ceasefire.

Operational impact:

- Commercial shipping through Hormuz remains high risk.

- Routing decisions continue to be driven by security exposure and war‑risk insurance acceptance, rather than navigational feasibility.

Red Sea & Bab El‑Mandeb – Risk Resurfacing

What changed this week:

- Houthi forces renewed warnings that Bab El‑Mandeb traffic could again be targeted should the Iran‑linked conflict escalate.

- Analysts are now cautioning against a dual‑chokepoint risk scenario, with Hormuz and Bab El‑Mandeb simultaneously constrained.

Operational impact:

- Asia–Europe routings via Suez remain volatile.

- Several carriers that had cautiously resumed Red Sea transits have already begun re‑routing vessels back around the Cape of Good Hope.

- These diversions add 10–14 days of sailing time and are creating secondary congestion at African bunkering and transshipment ports.

- Schedule reliability and destination ETA confidence continue to deteriorate.

Ocean freight – Current Status

Maritime conditions remain severely disrupted, despite the temporary ceasefire.

- Hormuz transits remain selective and clearance‑based.

- Red Sea and Bab El‑Mandeb routings are again viewed as high risk.

- Most major carriers continue to avoid Suez and Red Sea routings.

- Global schedule reliability, port congestion, and equipment imbalance continue to worsen.

At this stage, disruption is being absorbed primarily through cost escalation rather than capacity withdrawal, with services operating but at materially higher fuel‑ and risk‑adjusted cost levels.

Marine Insurance – War Risk Premiums

Despite the ceasefire, insurance conditions have not eased.

What changed this week:

- Insurers confirmed that war‑risk premiums will remain elevated.

- Reported premium levels include:

- 1–3% of vessel value per transit for most affected routings

- Up to 7% in extreme or high‑risk scenarios

- Several insurers have shortened quotation validity windows to as little as 24 hours.

Insurance acceptance continues to be a direct determinant of routing feasibility, voyage approval, and final cost.

Fuel Supply & Cost Pressure – Europe

Fuel remains a central operational and pricing risk.

- European jet fuel prices remain near record levels, reported at approximately USD 1,900 per metric ton.

- UK airports, including London Heathrow, remain among the most exposed.

- France remains the next most vulnerable market, although alternative sourcing offers partial mitigation.

- Eurocontrol continues to estimate that approximately 1,150 flights per day may remain impacted by rerouting throughout the summer.

Europe’s structural reliance on imported jet fuel (approximately 30% of demand) sustains sensitivity to ongoing disruption in the Strait of Hormuz.

Pricing & Surcharges – Market Impact

Operational disruption continues to translate directly into cost escalation:

- War Risk Surcharges remain in effect and under continuous review.

- Emergency Fuel Surcharges (EFS) continue to be rolled out or adjusted.

- Rate validity windows are shortening further.

- Premium pricing increasingly applies to time‑critical and capacity‑constrained shipments.

Pricing volatility remains high across both air and ocean freight.

Since our last update, fuel-driven cost pressure has intensified, and pricing volatility has increased further. Capacity constraints are also increasingly creating secondary effects beyond the immediate region, particularly across Asia–North America and Europe–North America corridors. While limited operational resumptions persist, they have not yet translated into a meaningful recovery at hub or network level.

Air freight – Capacity & Network Status

Air cargo operations in and around the Middle East remain severely constrained, despite limited resumptions by selected carriers.

- Selected Gulf carriers (including Emirates, Etihad, and Qatar Airways) have restarted restricted and tightly controlled operations, primarily for aircraft repositioning, repatriation movements, and pre-approved freighter services.

- These services remain subject to regulatory oversight, controlled corridors, fuel stops, and short-notice cancellations.

- The majority of belly and freighter capacity via traditional Gulf hubs remains unavailable for routine cargo planning.

- Dubai (DXB/DWC), Abu Dhabi (AUH), and Doha (DOH) cannot yet be considered reliable cargo hubs and continue to operate on a case-by-case approval basis.

- Air cargo capacity in the Middle East region remains approximately 30% below pre‑conflict levels.

Cargo operations across the UAE remain heavily pressured. Dubai (DXB/DWC) and Sharjah (SHJ) continue to experience persistent backlogs with limited recovery, while overflow pressure is increasingly affecting Abu Dhabi. Booking remains subject to carrier approval, and frequent last-minute schedule changes should be expected.

In parallel, additional surface transport limitations into Qatar are constraining road-based contingency options. Customers should not assume Gulf hub routings or cross-border trucking will function as fallback solutions.

Overall, air cargo capacity through the Gulf remains well below normal levels and should not be considered stable.

Middle East Airspace & Operational Environment

The regional operating environment remains fluid, fragmented, and capacity constrained, with continued operational and security volatility:

- Iran, Iraq, Kuwait, and Syria remain closed or effectively unavailable for routine civilian traffic.

- Israeli airspace remains highly restricted, with only limited, government-approved movements permitted.

- UAE and Qatari airspace are partially open via strictly controlled corridors, with restricted routings, capacity caps, and case-by-case approvals.

- Saudi Arabia and Oman remain critical transit corridors; however, both are operating under contingency routings and elevated air traffic control (ATC) load.

- Jordanian airspace remains restricted and subject to short-notice operational changes.

Across the region, openings and closures continue to evolve rapidly and, in some cases, on an hourly basis. Even where corridors remain technically open, operational reliability and uplift availability remain unstable and should not be assumed for routine planning.

Global Capacity Developments

The initial sharp drop in global air cargo capacity has partially recovered, supported by:

- Additional direct Asia–Europe services.

- Expanded use of integrator networks, charters, and ad hoc capacity.

However:

- Overall freighter availability remains constrained.

- Displaced aircraft are creating secondary congestion on Europe–North America lanes.

- Load factors remain high across most long-haul corridors.

- Rising fuel costs continue to exert upward pressure on pricing.

Any improvement remains fragile and subject to immediate reversal should the security situation deteriorate.

Alternative Gateways & Routings

With Middle East hubs still heavily constrained, the industry continues to rely on alternative gateways, including:

- Southern Europe

- Eastern Mediterranean

- North and East Africa

- Oman (Muscat – MCT), which continues to function as a primary relief and repositioning hub.

Please note:

- These routings typically involve multi-leg movements.

- Transit times are longer and less predictable.

- Capacity remains limited and competitive, often requiring advance commitment and premium pricing.

Corridor‑Specific Rate Pressure

The sharpest rate increases have been observed on South Asia and Southeast Asia outbound corridors, particularly towards the Middle East:

- Spot rates surged 50–100% in late March compared to four weeks earlier.

- Drivers include severe regional capacity shortages, heavy reliance on Middle Eastern carriers, sharply higher jet fuel prices, and newly introduced war‑risk surcharges.

Five weeks into the conflict, cost pressure has spread beyond Asia–EMEA:

- Airfreight rates from Northeast and Southeast Asia to North America have increased by mid‑ to high‑double digits.

- South Asia–North America rates have risen by approximately 75%, reflecting the role of Middle Eastern carriers on these lanes.

Any short‑term airfreight demand uplift resulting from ocean carriers declaring “end of voyage” at alternative ports is expected to be temporary, with recovery costs potentially offset by future demand softening.

Fuel Supply & Cost Pressure – Europe

Fuel has become a central risk factor for aviation:

- European jet fuel prices have reached record levels, reported at approximately USD 1,900 per metric ton.

- Airports in the UK, including London Heathrow, are viewed as the most exposed, with flight disruptions already observed.

- France is assessed as the next most vulnerable market, although alternative sourcing options exist.

- Eurocontrol estimates that ~1,150 flights per day may continue to be impacted by regrouting’s throughout the summer if current conditions persist.

Europe’s structural dependence on imported jet fuel (approximately 30% of demand) increases sensitivity to ongoing Strait of Hormuz disruptions.

Ocean freight – Current Status

Maritime conditions remain severely disrupted:

- The Strait of Hormuz remains effectively closed to most commercial shipping, with only highly selective, clearance-based transits observed.

- Major carriers have suspended or restricted Gulf services, and many shipments face diversions and revised discharge / port rotation decisions due to security and insurance constraints.

- Red Sea and Suez routings remain high-risk and widely avoided, with diversions via the Cape of Good Hope continuing.

- Schedule reliability, port congestion, and equipment imbalances continue to worsen globally.

While several ports in the UAE, Oman, Saudi Arabia, Egypt, and Jordan remain operational, routing and discharge decisions are increasingly driven by security exposure, war-risk insurance acceptance, and carrier network constraints.

At this stage, ocean freight disruption is being absorbed more through cost escalation than structural capacity loss: most services continue to operate, but at materially higher fuel-adjusted cost levels and with reduced schedule reliability.

Pricing & Surcharges – Market Impact

Operational disruption continues to translate into sustained cost increases, with further upward pressure expected as fuel surcharges and GRIs take effect.

In parallel, jet fuel availability and pricing have emerged as a material operational risk in Europe. Elevated fuel prices and constrained supply are beginning to affect airline scheduling decisions at major hubs, and continued rerouting and fuel sourcing constraints may sustain upward pressure on airfreight rates even outside Middle East-linked corridors.

Customers should anticipate continued volatility in airfreight pricing, with fuel-related surcharges subject to short-notice revision and limited validity windows. While demand has remained resilient to date, any prolonged escalation in fuel prices or broader economic fallout could begin to weigh on airfreight demand and alter current utilization dynamics.

In addition:

- War Risk Surcharges remain in effect and under continuous review

- Emergency fuel surcharges (EFS) are being rolled out by multiple carriers

- Premium pricing increasingly applies to time-critical and capacity-constrained shipments

While Middle Eastern Airlines have partially resumed operations for repatriation flights, we still advise avoiding cargo bookings to/via DXB, AUH, and DOH for the next few weeks. Cargo backlogs at these hubs remain severe and it may take weeks to clear or transit as of today.

Air freight – Capacity & Network Status

Air cargo operations in and around the Middle East remain severely constrained, despite limited resumptions this week:

- Selected Gulf carriers (including Emirates and Etihad) have restarted restricted and reduced flight schedules, primarily to repatriate passengers, reposition aircraft, and clear stranded backlogs

- These services are operating under strict regulatory oversight, reduced frequencies, fuel stops, and remain subject to short notice cancellation

- The majority of belly and freighter capacity through Gulf hubs remains unavailable for standard cargo planning

- Dubai (DXB/DWC), Abu Dhabi (AUH), and Doha (DOH) continue to be unreliable for routine cargo routings; movements are limited to approved, case by case operations only

Overall, air cargo capacity from affected Gulf hubs remains significantly below normal levels and cannot yet be considered stable.

Middle East Airspace & Operational Environment

The operating environment across the region remains fluid:

- UAE airspace is partially open via strictly controlled corridors, with capacity subject to ongoing military activity

- Qatari airspace remains closed, with no regular commercial cargo services operating

- Israeli airspace remains closed to routine civil aviation, with only limited, government approved freighter movements

- Airspaces over Iran and Iraq remain fully closed to civilian traffic

- Jordanian airspace is restricted, and conditions may change with little notice

Openings and closures continue to change rapidly and, in some cases, on an hourly basis.

Global Capacity Developments

The sharp initial drop in global air cargo capacity has partially recovered, supported by:

- Additional direct Asia–Europe services

- Expanded use of integrator and charter capacity

However:

- Overall freighter capacity remains reduced

- Displaced aircraft are creating secondary congestion on Europe–North America lanes

- Load factors remain high across most long haul corridors

Any improvement remains fragile and subject to immediate reversal should the security situation deteriorate further.

Alternative Gateways & Routings

With Middle East hubs still constrained, the industry continues to rely on alternative gateways, including:

- Eastern Mediterranean

- Southern Europe

- North and East Africa

- Oman (Muscat – MCT), which is currently serving as a primary relief and repatriation hub

Please note:

- These routings involve multi‑leg movements

- Transit times are longer and less predictable

- Capacity is limited and competitive, often requiring advance commitment and premium pricing

Ocean freight – Current Status

The ocean freight situation has further deteriorated:

- The Strait of Hormuz remains closed for commercial shipping

- Major carriers have suspended Gulf services, frozen bookings, or declared end‑of‑voyage for Middle East‑bound cargo

- Red Sea and Suez Canal routings remain unavailable, forcing diversions via the Cape of Good Hope

- Schedule reliability, port congestion, and equipment imbalances continue to increase

While several ports in the UAE, Oman, Saudi Arabia, Egypt, and Jordan remain operational, routing and discharge decisions are increasingly driven by security, insurance acceptance, and carrier network constraints.

Pricing & Surcharges – Market Impact

Operational disruption is translating into direct and sustained cost increases across air and ocean freight.

Ocean Freight – Freightos Baltic Index (Weekly)

- Asia – US West Coast: +10%

- Asia – US East Coast: 9%

- Asia – North Europe: +6%

- Asia – Mediterranean: +2%

Air Freight – Freightos Air Index (Weekly)

- China – North America: +11%

- China – North Europe: +2%

- North Europe – North America: 9%

In addition:

- War Risk Surcharges are being applied and remain under continuous review

- Fuel costs are rising, with additional Fuel Surcharges (FSC) expected

- Premium pricing is increasingly applied to time critical and capacity constrained shipments

Impact on logistics & supply chains

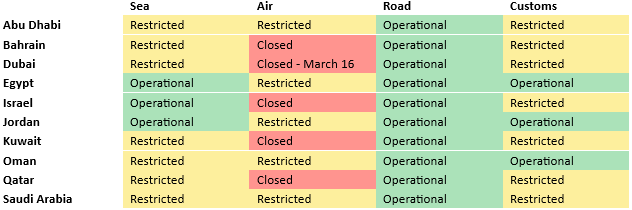

For airfreight we have seen sudden impacts due to airport closures in Middle East – where Dubai and Doha serve as major hubs, and when they close (and effectively Emirates and Qatar cancel all flights) this also impacts the trade between Asia and Europe. We see resumption in operations now so things are stabilizing. Below is the latest situation of port operations in Middle East – and as mentioned above, things can change by the hour.

Current state of operations at Middle East ports:

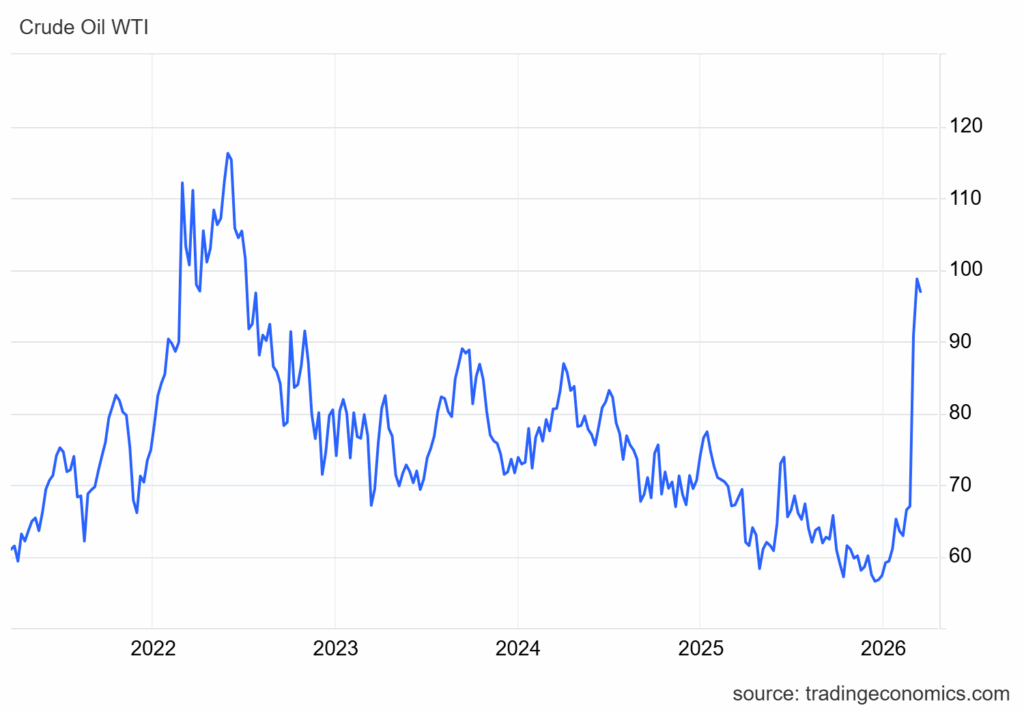

What impacts all modes of transport (air, ocean, trucking) is the oil price as it represents a major cost of their operation – where we have seen a spike.

Air freight update

Multiple sources confirm dramatic increases linked to airspace closures & capacity loss.

Key figures:

- Global airfreight rates up 6% week on week in early March, +3% YoY.

- Rates on South Asia → Europe lanes up as much as 70% since start of conflict.

Freightos Air Index:

- China → N. Europe +7% weekly

- China → N. America +2% weekly

- Europe → N. America +3% weekly

Indicative estimate vs. 28 Feb baseline:

- +20–40% globally, +50–70% on lanes using Middle East corridors.

Ocean freight update

Overall increases:

- Container rates have surged 14.9% week over week and 28.3% since just before airstrikes on Feb 27 based on SCFI index movements.

- Middle East lane rates up 40.8% in one week.

- War Risk Surcharges (WRS) applied by major carriers: USD 1,500–4,000 per container (global carriers including CMA-CGM, MSC).

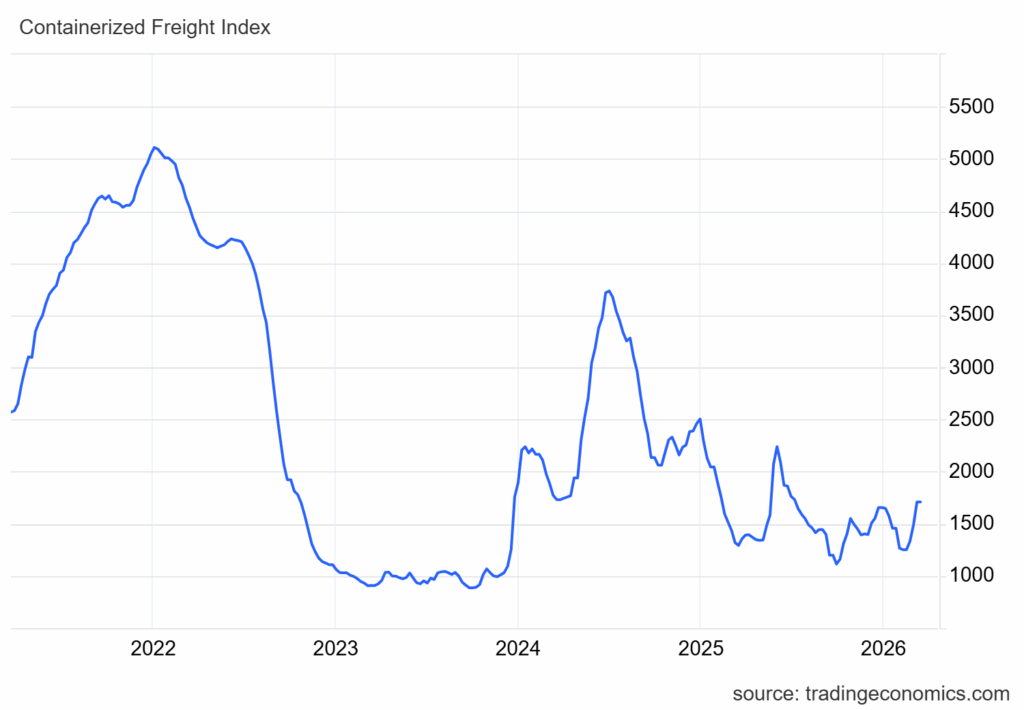

If you look at the container freight rate index over time – you can see that we are way below Covid levels:

Trucking/Road freight

War impact is primarily through diesel and energy markets.

Key figures:

- Diesel across EU spiked above €2/litre with strongest weekly jumps of 2026.

- Fuel spikes drive immediate cost increases; bunker fuel jumped 8.9% in one week, signaling broader transport cost escalation.

- European contract trucking rates were already rising due to capacity & driver shortages pre-war.

Indicative estimate vs. 28 Feb baseline:

- +8–12% trucking cost increase directly attributable to war driven fuel spikes.

Impact on logistics & supply chains

These developments are affecting global freight flows:

Air freight update

Current situation

- Several airlines have suspended services and stopped accepting cargo to key Middle East destinations.

- Airspace restrictions are forcing airlines to reroute flights, increasing transit times.

- Available airfreight capacity has been significantly reduced across the region.

- Major regional hubs including Dubai, Abu Dhabi, and Qatar are operating under restricted schedules.

- Air freight rates are increasing due to reduced freighter capacity and longer routings.

- War risk surcharges and fuel surcharges are being applied by several carriers.

- Spot rate volatility is expected for urgent and premium shipments.

Customer impact

- Customers may experience limited space availability and delays.

- Transit times may increase due to rerouting and operational constraints.

- Upward pressure on spot rates.

- Possible schedule adjustments and longer transit times.

Ocean freight update

Current situation

- Carriers continue to avoid the Red Sea and Suez Canal due to ongoing instability.

- The Strait of Hormuz is fully closed to commercial shipping.

- Vessels are being rerouted via the Cape of Good Hope, increasing transit times and operational costs.

- Major shipping lines have paused or adjusted services in the Gulf region.

- War Risk and Emergency Conflict Surcharges have been introduced.

Customer impact

- Extended transit times (Cape routing may add 10–15 days).

- Schedule disruptions.

- Equipment imbalances.

- Additional surcharges for Gulf and Red Sea cargo.

- Temporary booking restrictions on selected Middle East destinations.

- Potential cargo redirection to alternative ports for final delivery.

Fuel market developments

Energy markets have reacted strongly to the escalation in the Middle East.

- Fuel prices have increased sharply, putting additional pressure on airline operations.

- Oil prices have risen significantly amid concerns about supply disruptions and restricted shipping through the Strait of Hormuz.

- Brent crude briefly surged above $100 per barrel before stabilizing at elevated levels.

- Fuel markets remain highly volatile, with potential implications for aviation fuel, diesel, and bunker prices.

Expected impact

- Potential BAF (Bunker Adjustment Factor) increases

- Higher airline fuel costs affecting airfreight rates

- Upward pressure on overall logistics cost